BEYOND THE NUMBERS

Reforming Tax Deductions Would Improve Economic Efficiency and Raise Needed Revenue

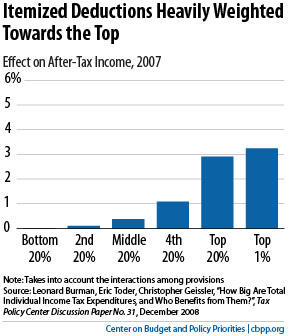

The Wall Street Journal opposes the idea of reducing the value of itemized deductions for high-income taxpayers to help reduce deficits, but it ignores a basic reality: these deductions are economically inefficient. Reforming them would improve efficiency as well as raise much-needed revenue, so that should be front and center in deficit-reduction negotiations.

Take the mortgage interest deduction as an example:

- An affluent investment banker who has a $1 million mortgage and pays $40,000 in mortgage interest each year receives a housing subsidy of $14,000 annually. The banker pays 65 cents of every dollar of mortgage interest, and taxpayers pick up the remaining 35 cents.

- By contrast, a typical middle-class family, such as a welder or a nurse making $60,000 and paying $10,000 a year in mortgage interest on a more modest home, receives a housing subsidy worth $1,500 annually. Here, the family pays 85 cents of every dollar of mortgage interest and taxpayers pick up just 15 cents.

It’s both inefficient and inequitable for taxpayers to pay 15 percent of the middle-class family’s mortgage interest but one-third of the investment banker’s.

Both the bipartisan Bowles-Simpson commission and the bipartisan Rivlin-Domenici commission recognized this glaring design flaw and advanced reform proposals that improve efficiency and raise much-needed revenue. So has the President.

Budget negotiators would be well served to put these proposals in the middle of the negotiating table.