BEYOND THE NUMBERS

Orszag: Ryan Budget Would Increase Total Health Care Spending

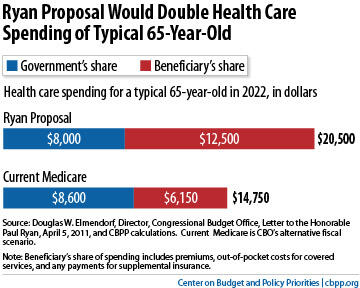

In a new Bloomberg column, former OMB Director Peter Orszag explains how House Budget Committee Chairman Paul Ryan’s plan to privatize Medicare would increase total health care spending. I made the same point recently; below is the chart in my post.

There are two reasons why. First, private insurance plans have much higher administrative costs than Medicare. Second, private plans have less bargaining power with health care providers and are unable to negotiate payment rates that are as low as Medicare’s.

Orszag concludes with the following message to policymakers who initially supported the Ryan plan but are now reconsidering because of its unpopularity with voters: “If your goal is to reduce health care spending significantly, you can safely retreat from [the plan] on its substance.”