BEYOND THE NUMBERS

How to Shore Up Social Security

We pointed out yesterday that Social Security faces a significant, but manageable, shortfall, as we explain in our just-released annual analysis of the Social Security trustees’ report. Here’s how policymakers should plan to fill the gap.

Although the combined trust funds won’t face depletion for another two decades — and even then the program could pay three-fourths of scheduled benefits — lawmakers should address the shortfall reasonably soon so the program can fully meet its promises. Prompt action would permit changes that are gradual rather than sudden, and allow people to plan their work, savings, and retirement with greater certainty.

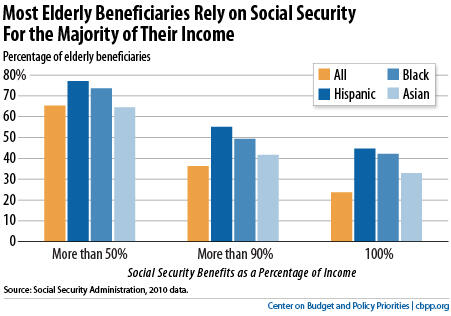

As policymakers consider their options, they should keep a few key facts in mind. Nearly every American participates in Social Security, first as a worker and eventually as a beneficiary. Its benefits are the foundation of income security in old age, though they’re modest both in dollar terms (elderly retirees and widows receive an average Social Security benefit of $15,000 a year) and when compared with benefits in other countries. Millions of beneficiaries have no income other than Social Security (see chart).

Because Social Security benefits are so modest and make up the principal source of income for most recipients, policymakers should restore solvency through a mix of revenue increases and benefit changes, with increased revenues contributing at least half — and preferably more — of the savings. Revenues could come from raising the maximum amount of wages subject to the payroll tax (which now encompasses only about 83 percent of covered earnings, well short of the 90 percent figure envisioned in the 1977 Social Security amendments); broadening the tax base by subjecting voluntary salary-reduction plans, such as cafeteria plans and health care Flexible Spending Accounts, to the payroll tax (as 401(k) plans and similar retirement accounts are); and gradually raising the payroll tax rate.

Future workers will be more prosperous than today’s. The trustees project that the average worker will be almost 50 percent better off — in real terms — in 2040 than in 2013, and twice as well off by 2070. It’s appropriate to devote a small portion of those gains to financing Social Security, while still leaving future workers with much higher take-home pay. Social Security is a popular program, and poll respondents of all ages and incomes express a willingness to support it through higher taxes.

One deadline for action is approaching more quickly. Policymakers will have to replenish the Disability Insurance trust fund by 2016. They should try to do so as part of a comprehensive and balanced solvency package, because the retirement and disability components of Social Security are closely woven together. But if they don’t accomplish that in time, it’s reasonable to reallocate taxes between the disability and retirement programs, as policymakers have often done in the past.

Social Security is the most effective and successful income-security program in the nation’s history. Policymakers should design reforms judiciously so that it remains that way.