BEYOND THE NUMBERS

House Republicans’ Wrong-Headed Approach to Tax Extenders

House Republicans are putting before the House this week a campaign-oriented bill of wide-ranging measures that have previously passed the House, including repealing portions of the Affordable Care Act and scaling back Dodd-Frank regulations. The bill, which won’t advance beyond the House due to obvious Senate and White House opposition, also includes business tax provisions that lawmakers will likely consider again during Congress’ post-election lame duck session this fall. For that reason alone, the legislation warrants some attention.

The House bill would make permanent certain “

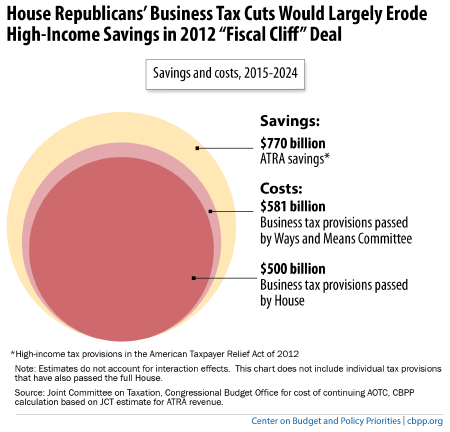

” — so named because Congress routinely extends them for a year or two at a time — as well as bonus depreciation, which lets businesses take larger upfront tax deductions for certain purchases, such as machinery and equipment, and that historically has been a temporary measure to help revive a weak economy. Congress should reject the House approach to these provisions because it is not fiscally responsible, is poorly designed from an economic standpoint, and is antithetical to tax reform. Moreover, it reflects seriously misplaced priorities, putting the permanent extension of these business provisions ahead of more pressing provisions for hard-working families.- Its $500 billion price tag is fiscally irresponsible. Policymakers have enacted significant deficit-reduction measures since 2010, with the vast majority coming from spending cuts. The one revenue contribution stems from the 2012 “fiscal cliff” bill — i.e., the American Taxpayer Relief Act — that raised $770 billion in revenue from high-income taxpayers (from 2015 to 2024). The tax extenders and bonus depreciation provisions in the House bill would reduce revenue by $500 billion over the decade, effectively giving back two-thirds of the revenue contribution to deficit reduction (see chart). (The total cost of the House bill is about $575 billion, because of other revenue-losing provisions.)

Image

- It’s poorly designed from an economic standpoint because it makes bonus depreciation permanent. Making bonus depreciation permanent accounts for more than half of the $500 billion cost of the business tax provisions. But bonus depreciation was specifically designed not to be permanent because its temporary nature is what drives its (albeit limited) effectiveness during recessions. Its modest economic boost comes entirely from inducing firms to accelerate some of their purchases into the period when the tax break is in effect and the economy is weak. Making it permanent would negate this modest incentive effect. That’s why the Bush Administration and Congress allowed it to expire after the 2001 recession ended and why this Congress should let it expire now.

- It moves away from tax reform. The fundamental nature of tax reform is to “broaden the base” by scaling back tax subsidies and to use the freed-up funds to lower tax rates, reduce budget deficits, or both. For example, House Ways and Means Chairman Dave Camp (R-MI) earlier this year advanced a comprehensive plan that eliminated tax subsidies for certain business investments, including the repeal of bonus depreciation. These changes were central to his base-broadening provisions. But the package that House Republicans are now bringing before the House goes in the opposite direction. Its provision to make bonus depreciation permanent narrows the tax base and, thereby, moves away from tax reform.

If, during the lame duck session, policymakers consider making any tax extenders permanent, they should focus first on making permanent important provisions of the Earned Income Tax Credit (EITC) and Child Tax Credit (CTC) that are due to expire at the end of 2017. Failure to make the EITC and CTC provisions permanent would have a significant impact on low- and moderate-income families, pushing 17 million people (including 8 million children) into — or deeper into — poverty.