BEYOND THE NUMBERS

A Broken Promise Is Better Than a Broken Economy

President Obama pledged to cut the deficit in half in his first term. It’s a good thing he didn’t keep that promise or we’d be looking at a much weaker economy.

Faced with a tanking economy and a surging budget deficit upon taking office in 2009, President Obama and Congress quickly enacted policies that greatly expanded deficits in the short term in order to help stabilize the economy.

That’s a sound approach — and it worked.

The 2009 Recovery Act and other aggressive monetary and fiscal policies enacted in late 2008 and 2009 will have only a tiny impact on long-term deficits, and they may well have prevented another Great Depression.

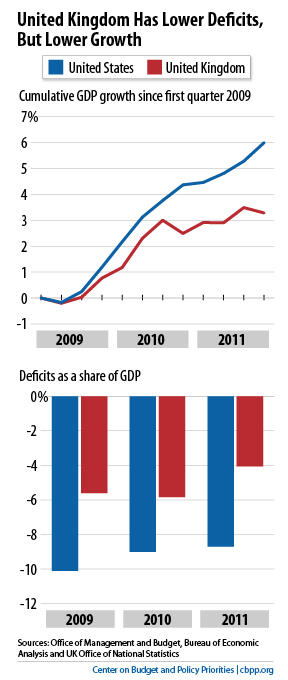

As we’ve documented in our chart book, the legacy of the Great Recession has been a stubbornly slow recovery. It is unfortunate that policymakers did not enact a well-thought-out second round of stimulus at the beginning of 2010, and the last minute tax cut/unemployment-insurance compromise they worked out at the end of the year was far from ideal. But contrast the U.S. experience with what has happened in the United Kingdom and the Eurozone, where policymakers bought into the misguided notion (which many Republicans here share) that the path to prosperity begins with fiscal austerity.

Austerity hasn’t been working out well. As the charts show, deficits have been smaller and fallen faster in the United Kingdom than the United States since 2009, but the U.S. economy has grown more, while the U.K. economy is faltering.

It’s true that the new Obama budget’s projected 2013 deficit of $901 billion (5.5 percent of GDP) is more than half of the projected 2009 deficit of $1.2 trillion (8.3 percent of GDP) that he inherited. But the budget includes proposals that would make significant progress in reducing deficits over the next ten years — although we’ll need to do more, especially for future decades.

In particular, under its economic assumptions, the Obama budget would achieve what most budget analysts, and all recent bipartisan panels, have identified as the crucial fiscal goal for the decade ahead: stabilizing the debt so that it no longer rises faster than the economy. It would cut the deficit to 3.9 percent of GDP in 2014, less than half the size of the 2009 deficit, and to below 3 percent of GDP by 2018. (The Congressional Budget Office assumes somewhat slower economic growth and thus will likely have somewhat higher numbers than these in its March analysis of the President’s budget.)

The United States has not pursued the ideal approach of enacting policies that increase the deficit in the short run in order to support the weak economy while simultaneously enacting deficit-reduction policies that kick in several years later, when the economy is stronger. But the contrast with the European experience strongly suggests that providing support for a weak economy without specifying how to pay for it later is far better than not providing support at all.